The true cost of debt includes the interest rate alongside hidden fees, tax implications, and the significant opportunity cost of lost potential investments. It also encompasses non-financial burdens such as chronic stress, mental health challenges, and reduced flexibility in personal or business decision-making. Understanding these combined factors allows for a more accurate assessment of how borrowing impacts overall financial and emotional health.

Many professionals view debt through the narrow lens of interest rates and monthly installments; however, focusing solely on these figures ignores the silent erosion of your long-term wealth and strategic flexibility. When your capital is anchored to past obligations, you lose the agility required to navigate new opportunities. This hidden burden creates a psychological weight that can cloud your judgment and strain your most vital relationships. In this analysis, we will explore the multifaceted reality of borrowing beyond the surface level. We will examine the heavy opportunity costs of debt, discuss Warren Buffett’s perspective on leverage, and address the emotional toll that financial obligations exert on your well-being. By understanding these invisible factors, you can effectively recalculate your financial trajectory and reclaim the independence necessary to steer your future with confidence.

The Visible Cost: Why Interest Rates Only Tell Half the Story

Most borrowers view debt through the narrow lens of the Annual Percentage Rate (APR). However, the true cost of debt is a multidimensional burden that begins with the math but quickly expands into your broader financial health. While the interest rate is the most visible figure, it is often obscured by loan origination fees, late payment penalties, and recurring service charges that quietly inflate the total amount you repay over the life of the loan.

The math becomes more punishing when you consider the difference between before-tax and after-tax costs. Most personal debt is serviced with after-tax dollars, meaning you have already paid the government before you pay your creditors. If you are in a 22 percent federal tax bracket, you must earn approximately $1.28 in gross income for every $1.00 you send to a lender. This disparity represents a significant drain on your household take-home pay that is never reflected on a standard loan statement.

Beyond these direct fees, high-interest debt, particularly from credit cards, utilizes compounding interest against you. Unlike simple interest, credit card balances often compound daily; you are effectively paying interest on previous interest, creating a cycle that erodes your net worth. Furthermore, every dollar allocated to debt service is a dollar lost to tax-advantaged growth. When you prioritize debt over a 401(k) or IRA contribution, the true cost includes the decades of compound growth you have forfeited. Understanding these layers is essential for any Financial Decision Making Guide and helps you answer 8 Honest Questions to Ask Yourself at a Crossroads regarding your financial direction.

The Opportunity Cost: What Your Future Self Is Giving Up

While the math of interest rates is sobering, the most significant component of the true cost of debt is opportunity cost. In economic terms, this represents the value of the next-best alternative you forfeit when you make a choice. Every dollar you send to a creditor is a dollar that cannot be directed toward a 401(k), a home down payment, or a child’s college fund. When you carry a balance, you are effectively trading your future wealth for today's consumption.

Consider a practical scenario to visualize this weight. If you pay $500 per month in interest alone for 10 years, you will have handed $60,000 to your lender. However, if you had invested that same $500 monthly into an S&P 500 index fund with an average annual return of 8 percent, you would have accumulated approximately $91,000. The true cost of debt in this instance is not just the $60,000 in interest payments; it is the $91,000 in wealth that your future self no longer possesses. This $31,000 gap is the hidden price of missed potential.

Debt also creates a state of locked equity. This term describes how your financial flexibility is restricted because your assets and future income are already pledged to others. Locked equity prevents you from seizing new opportunities, such as starting a business or moving for a better job, because your margin of safety is depleted. When you are navigating life's transitions, this lack of maneuverability can be paralyzing. Using a Financial Decision Making Guide helps clarify these trade-offs before they become permanent burdens.

Understanding this weight is part of answering the 8 Honest Questions to Ask Yourself at a Crossroads. It is not about feeling shame for past choices; it is about recognizing that debt is a claim on your future time and energy. By quantifying what you are giving up, you can begin to make more informed decisions about how to reclaim your financial direction.

The Warren Buffett Perspective: Lessons from the Oracle of Omaha

Warren Buffett, the Oracle of Omaha, offers a perspective on the true cost of debt that centers on the preservation of opportunity. He has often observed that if you are smart, you are going to make a lot of money without borrowing. Buffett’s primary warning is that leverage is the only way a smart person can truly go broke; it removes your ability to stay the course when markets or life circumstances become volatile. While his company may use debt strategically in a corporate context, his advice for individual households is significantly more conservative.

For most people, debt represents a backwards way of living that swaps tomorrow’s freedom for today’s consumption. It forces a person into a defensive posture where they must work to satisfy past choices rather than fund future goals. This loss of autonomy is why our Financial Decision Making Guide stresses the importance of liquidity and capital preservation. Evaluating your position through the 8 Honest Questions to Ask Yourself at a Crossroads can help you determine if your current liabilities are a temporary tool or a permanent barrier to the independence Buffett champions. By avoiding the trap of leverage, you maintain the flexibility required to navigate life's inevitable shifts.

The Emotional Weight: Understanding Debt Stress and Mental Health

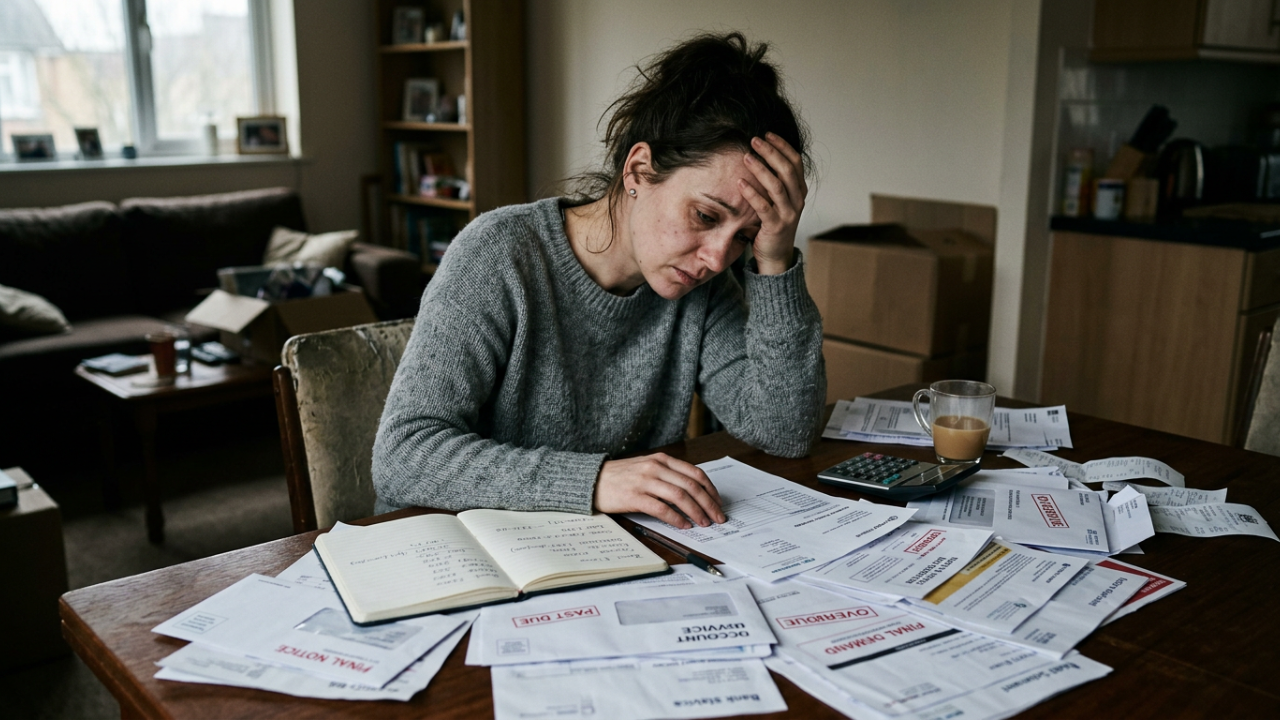

While the Oracle of Omaha highlights the loss of autonomy, the true cost of debt for many individuals is the quiet erosion of mental peace. Clinicians and researchers often refer to "Debt Stress Syndrome" to describe the specific psychological toll of carrying persistent liabilities. Unlike an acute financial shock, such as a one-time emergency expense, debt functions as a chronic stressor that shapes your daily mental baseline. It is a lingering weight that does not disappear when the workday ends; instead, it often manifests as sleep deprivation, clinical anxiety, and a higher susceptibility to depression.

The Psychology of Debt explains why different types of liabilities carry varied emotional weights. For instance, you might view a student loan as a productive investment in your human capital, while high-interest credit card debt often feels like a stagnant reminder of past consumption. This distinction is vital because the heavier the emotional weight, the more it fuels "short-termism." This is a survival-based mindset where your brain prioritizes immediate relief or avoidance over long-term strategic growth. This cognitive load effectively shrinks your perspective, making it difficult to navigate life’s transitions with a sense of agency.

When you are standing at a crossroads, the chronic stress of debt can make a necessary career change or a relocation feel like an impossible risk. It forces a defensive posture that clouds your judgment and often leads to panic-based choices. Utilizing a Financial Decision Making Guide is a practical way to reintroduce objectivity into a situation currently governed by stress. By confronting the reality of your situation through 8 Honest Questions to Ask Yourself at a Crossroads, you can begin to separate your identity from your balance sheet. Recognizing that debt is a lingering stressor, rather than a permanent character trait, is the first step in reclaiming the mental clarity needed to move toward a more stable future.

Strained Connections: How Debt Affects Relationships and Shared Goals

The psychological burden of debt rarely stays confined to the individual; it inevitably spills over into the most intimate areas of our lives. One of the most damaging aspects of the true cost of debt is its potential to erode the foundation of a partnership through financial infidelity. This occurs when one partner hides balances, credit cards, or expenditures from the other. Research consistently identifies money problems as a leading cause of divorce, and secretive debt is often the primary catalyst. When a spouse discovers hidden liabilities, the damage is seldom about the dollar amount alone. Instead, the loss of trust creates a rift that can be harder to repair than the financial balance itself.

Debt acts much like a restrictive covenant in a corporate loan agreement. In business, these covenants limit a company's operational flexibility, often preventing it from pursuing new investments or requiring a specific cash reserve. For a family, debt creates similar restrictions on lifestyle and shared goals. These "family covenants" dictate where you can vacation, what kind of home you can afford, and how you prepare for your children's future. They effectively outsource your decision making to your creditors, removing your ability to dream as a unit.

Reclaiming your shared direction requires a transition from secrecy to transparency. Utilizing a Financial Decision Making Guide can help couples map out a path forward based on objective data rather than emotion. Confronting the reality of your situation by asking 8 Honest Questions to Ask Yourself at a Crossroads can transform debt from a source of conflict into a shared project. Honesty is the first practical step toward rebuilding trust and ensuring that your future goals are no longer held hostage by past choices.

Taking Action: How to Recalculate Your Path Forward

Shifting from the damage to relationships toward personal reclamation requires an objective audit. To recalculate your path, you must move beyond the balance statement and quantify the impact on your most limited resource: time. Use this checklist to determine your personal true cost of debt:

Calculate the Labor Cost: Divide your total monthly debt payment by your net hourly take-home pay. Ask yourself: How many hours of work does this monthly payment represent? Is the original purchase worth the 15 or 20 hours of labor you must perform every month just to satisfy the creditor?

Identify the Deferred Dream: Explicitly name the goal you are currently delaying. If you are paying $400 a month toward high-interest balances, you are essentially paying a $4,800 annual "delay fee" on a career pivot, a home down payment, or a necessary sabbatical.

The Identity Audit: Practice separating your identity from your debt. Acknowledge that a balance is a mathematical reality to be solved, not a reflection of your character or intelligence. This cognitive shift reduces the paralysis of shame.

By viewing your liabilities through a Financial Decision Making Guide, you can strip away the emotional static that leads to panic-based choices. This moment represents a crossroads; it is the point where you stop looking at what was spent and start looking at what can be reclaimed. Answering the 8 Honest Questions to Ask Yourself at a Crossroads will help you define a new direction that prioritizes your future autonomy over past obligations.

Understanding the full cost of debt involves looking past the numbers to see how it impacts your peace of mind and future choices. While awareness is a vital first step, taking action can feel overwhelming. If you want expert help as you navigate your financial journey, our team is here to support you. You can find more detailed information and strategies in our Guides to help you regain control. Reaching financial freedom is a path you do not have to walk alone.